CHINA – PAKISTAN ECONOMIC CORRIDOR (CPEC): A WIN-WIN PROJECT

South Asia has traditionally been a region of political contest and a playing field for great games for multiple reasons. It was a source of wealth for British Empire in 18th /19th centuries, while during Cold War period (2nd half of 20th Century) it witnessed fierce rivalry between former USSR and US led West. Recent past also witnessed US led NATO presence in Afghanistan for some stated /unstated strategic motives. US so to say exit from the region is beginning of yet another contest for space /influence. The region will thus continue to experience a state of strategic flux and aggressive competition.

A new form of ‘Cold War’ or ‘Containment’ is taking roots in South Asia, reconfigured by US Asia Pivot Policy. Notwithstanding the wide spread poverty, geo-ethnic diversity and numerous territorial disputes making it a volatile and dangerous region, South Asia would witness emergence of at least two economic giants in next two decades. The prospects of global peace and prosperity would invariably be determined here in South Asia. The central and most effective role will, however, still continued to be played by US and China. Their interrelationship has begun to change from non-confrontational to competition; unless it gets transformed to a cooperative framework, South Asia is likely to remain embroiled in a Cold War or may drift towards overt hostility.

Pakistan’s geo strategic location as a hub of South Asia is a constant of geography. In words of Stephen P Cohn; “While history has been unkind to Pakistan, its geography has been its greatest benefit. It has resource rich area in the north-west, people rich in the north-east.[1]“Pakistan provides shortest and most economical trade routes to the emerging economic pivots of the World; to China for her trade with West, Gulf Region and India, and to India for her trade with Afghanistan, CARs and China. It also offers to CARs and Afghanistan, the access to warm waters for their trade with rest of the World. Apart from a Regional Transit Trade Hub, Pakistan’s strategic relevance gets further enhanced due to its close proximity to Vital Sea Lines of Communication (SLOCs) of energy /trade. Pakistan thus forms the gateway to several strategic directions, making it an area of enduring focus for World powers with often competing interests.

Ironically, this geo strategic advantage has been a perpetual burden, as Pakistan continues to muddle through security /stability issues, some of its own making while others imposed by external actors (regional /international); including some of its stated friends. Nevertheless, to benefit optimally from its geo-strategic significance, an efficient and well-connected communication system with futuristic and competitive outlook is imperative; answer lies in CPEC.

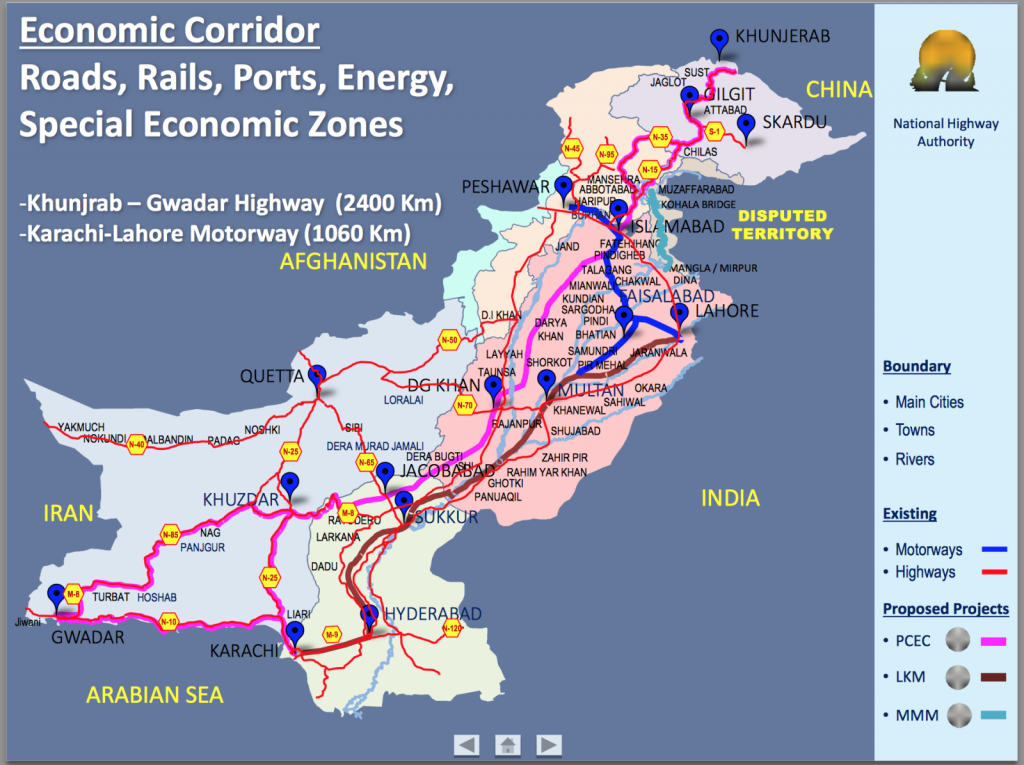

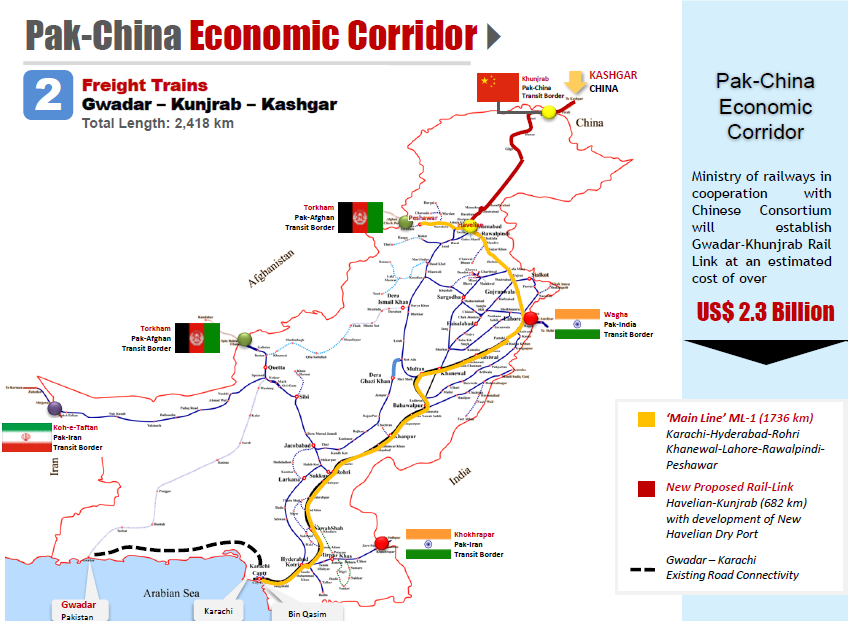

CPEC essentially has three tiers (Figure 1[2]); at first, Kashgar and Gwadar would be connected through highways /motorways, while at the second, through establishment of rail network (Figure 2[3]) and at third tier linked via energy pipeline and establishment of an oil refinery at Gwadar. In addition to establishment of EZs along the corridor, freight terminals /industrial parks would be established at Sust, Gilgit, Abbottabad, Loralai, Kohlu, Dera Ghazi Khan, Bhakkar, Rajanpur, Kashmore, Jacobabad, Khuzdar, Basima, Panjgur, Turbat and Gwadar[4].

On the international plane, Pakistan’s biggest challenge however, continues to be, reduced strategic space and the compulsion to manage own interests within a cooperative framework, while remaining relevant to key international players.

What’s in it for China

Chinese objectives are not entirely altruistic. Their strategy is driven by self-interests in the developing world which provide them the sources for their blooming industry and the growing markets like India, Gulf Region, Africa and even Latin America. Since 2012 China is the leading economy with a World market share of 18.34 % (2020); her merchandize exports amounted to USD 17.9 Trillion[5], way ahead of US.

As per World Bank statistics of 2018, Chinese trade with countries from Middle East & North Africa staggers around USD 290 Bn, with Europe & Central Asia around USD 918 Bn, with Latin America & Caribbean around USD 805 Bn, North America around USD 699 Bn, Iran USD 35 Bn, Iraq USD 30.4 Bn, Israel USD 14 Bn, Jordon USD 3.18 Bn, Lebanon USD 2 Bn, Syria USD 0.68 Bn and Turkey USD 21.5 Bn. In the immediate neighbourhood, Chinese trade with India was around USD 96 Bn, while with Afghanistan it was around USD 0.69 Bn and with Pakistan around USD 19 Bn. When accumulated, the total figure comes around USD 3 Trillion (2934 Bn). Even 25 % of this volume of trade transiting through Pakistan can have huge impact on Pakistan’s economy.

To ascertain the volume of savings, some of the distances are tabulated below[6]:-

| Table 1: Saving in terms of Distances (Via Shanghai vs. Gwadar) | ||||||

| Ser | From | To | Via Shanghai (miles) | Via Pakistan (miles) | Saved (miles) | Saved

(% age) |

| a | Central China | Middle East | 11206 | 3626 | 7580 | 68 |

| b | Central China | Europe | 17801 | 10928 | 6873 | 39 |

| c | Central China | Pakistan (Gwadar) | 10601 | 3081 | 7520 | 71 |

| d | Western China | Middle East | 12537 | 2295 | 10242 | 82 |

| e | Western China | Europe | 19132 | 9597 | 9535 | 50 |

| f | Western China | Pakistan (Gwadar) | 11932 | 1750 | 10182 | 85 |

Western Chinese provinces once connected to Pakistani ports through rail /road network (Figure 3[7]) would provide a jump off point to Chinese trade with the West, Africa and the Gulf Region (Figure 4[8]: 33 % of Container Traffic), curtailing the travel distance by 50 – 85 % (Table 1).

Out of China’s annual container trade of 225 Bn containers (2014), 30 % (67.5 M containers) is with European nations[9] and around 6 % with Africa. It may not be possible to handle the entire Chinese transit trade through Pakistan for obvious capacity reasons; even 10 – 15% share of container flow will have tremendous impact on Pakistan’s economy.

China is Pakistan’s third largest trading partner after US and EU, and has been the largest investor country in Pakistan, mostly in the development of communication infrastructure. Around 120 Chinese companies are doing business in Pakistan, while in energy sector 15 Power Projects (including hydel, thermal and nuclear) are being built by Chinese companies. China – Pakistan bilateral trade crossed US $19 B in 2018.

According to a Xinhua Report, Pakistan and China have agreed to work on laying of pipeline for transportation of crude oil from Gwadar to western China (via Khunjrab Pass, around 3600 km); currently China’s 50% of oil imported is supplied via Dubai – Shanghai – Urumqi (around 16,000 km).

China has obvious concerns over US increased presence in Asia Pacific Region along maritime chokepoints. It is here, Pakistan serves as China’s insurance policy providing alternative route bypassing these chokepoints for its trade with Middle East, Africa and the West. Pakistan is thus undeniably at a privileged position in Chinese Global Matrix when viewed from both the perspectives of trade and security.

What India is Missing!

India’s actions as “BIG POWER” as opposed to “GREAT POWER” continue to induce instability manifested through indirect strategies. Indian aspirations are aimed at acquiring regional economic and military power status transiting to global stature. With support from US lead allies, India is being promoted as a counter weight to China; notwithstanding wide gaps between intent and capacity. Indian intelligentsia feels that it has never been afforded its due stature at regional and global level. It seeks to cash onto the opportunity offered by US exit from Afghanistan, offering its promising domestic market; Indian diaspora in the West and Middle East is acting as a catalyst. In the strategic domain, India considers Pakistan as the sole obstacle obstructing her quest for regional hegemony.

For FY 2018 as per World Bank statistics, India’s trade with China was around USD 95.73 Bn, with Iran the mutual trade staggers around USD 21 Bn, with Pakistan around USD 2.98 Bn and with Afghanistan despite all rhetoric trade was around USD 1.24 Bn. With CARs it stands at USD 500 M[10].

Pakistan in itself is also a large consumer market of over 200 M people. Informal trade with India via other channels /routes ranges between USD 250 M to 3 Bn; 88 % of it takes place via Dubai; potential is however 10 – 20 times greater. India on the other hand needs uninterrupted and assured supply of energy from Central Asia and ME for its industry to maintain desired economic growth. The potential of transit of mineral fuels through Pakistan is estimated around USD 10.4 to 10.7 Bn[11].

With CPEC connecting Gwadar with Kashgar, Pakistan will have the option of bypassing Afghanistan to reach CARs like Kazakhstan, Kyrgyzstan and Tajikistan. Notwithstanding, Indian investment of over USD 100 M on Chahbahar project connecting it with Afghanistan border and around USD 10.8 Bn investment within Afghanistan till 2012, attempts to bypass Pakistan for its trade with CARs and Afghanistan would be cost prohibitive. Iran connection may not be economically viable and sustainable in long run.

Notwithstanding, the traditional animosity between Pakistan and India, current global trade patterns driven by globalization and liberalization of economy demand mutual cooperation and trade. Apart from being a promising large market itself, Pakistan offers India land access to the markets of CARs, Afghanistan and Iran. Gwadar – Kashgar link further extended to CARs of Tajikistan, Kyrgyzstan, Kazakhstan and possibly Uzbekistan would offer much greater opportunities to India also, avoiding perpetually instable Afghanistan. This can become a reality, provided India is ready to part with her hegemonic biases and makes decisions purely driven by geo-economic considerations. Indian growing energy demands also necessitate access to the energy source regions of Central Asia, Iran and Middle East through Pakistan. Both sides will have to resolve their outstanding disputes or at least work out an arrangement where they can trade with each other as well as other neighbours in the region.

Reasserting Russia – Rapprochement with Pakistan

Enhanced engagements in the domains of security /economics and increased Russian activism may be the beginning of yet another Cold War, albeit with different allies. Russia – China gas deal worth US $ 400 B, signed in May 2014 and around 40 agreements in various sectors including energy and infrastructure signed during Chinese Premier’s visit to Russia in October 2014 also demonstrate her intent and resolve in face of sanctions by US and EU over Ukraine episode.

Notwithstanding, historically cold relations Russian rapprochement with Pakistan manifested by recent exchange of high level military visits and joint exercises with Pakistan Army and Navy is a win-win opportunity for both countries. Karachi Steel mill is a testimony of Russian expertise in heavy industries, its revival can be a starting point for renewal of mutual relations; there is tremendous potential for joint ventures /cooperation. Russia may eventually get connected with planned CPEC in mid to long term and accomplish her erstwhile quest of gaining access to warm waters for trade.

CARs

These resource rich landlocked countries are desperately seeking markets for flow of their energy reserves and are looking beyond immediate neighborhood. Pakistan lies on the fringes of Central Asia; closest CAR is Tajikistan which is merely separated by a narrow Wakhan Corridor. In addition to maintaining historical and cultural linkages with this region, Pakistan offers shortest land route to CARs for access to the Arabian Sea /Indian Ocean for their trade; 2600 km as compared to Iran (4500 km) or Turkey (5000 km)[12].

Interestingly, CPEC further connected with Tajikistan, Kyrgyzstan, Kazakhstan and Uzbekistan would provide a lucrative detour making Afghanistan irrelevant. Pakistani businessmen have exported goods to Almaty on the same route[13] under Quadrilateral Trade Agreement between China, Kyrgyzstan, Tajikistan and Kazakhstan (operational since 2004). Pakistan is also a signatory of Central Asia Regional Economic Cooperation (CAREC).

Pakistan also seeks natural gas from Central Asia and supports the development of pipelines from the region; TAPI gas pipeline would transport 30 BCF of natural gas annually over distance of 1700 km. There is also an alternative project namely TKPI (Termez[14], Kabul, Peshawar, Islamabad) which would traverse a distance of 750 km (nearly half of TAPI) to reach Islamabad[15]. It can be extended from Lahore to Amritsar (India) adding 250 km, if required. Amu Darya Basin of Uzbekistan contains 15.6 TCF (possibly up to 36.5 TCF) of natural gas and 1.6 Bn Barrels (possibly up to 3.6 Bn Barrels) of oil reserves[16]. However, actualization of these projects remains linked with peace and stability in Afghanistan.

Afghanistan – Pakistan Equation

Afghanistan being a victim of “Great Games” has witnessed perpetual instability since couple of centuries at least. It is an important neighbour to Pakistan with strong historical, cultural and ethnic bonds. Instability in Afghanistan, due to overlap of geography, history and culture has induced instability in the frontier regions of Pakistan as well. Pakistan has been struggling all along to manage this instability albeit at a heavy cost.

Traditionally, stability in Afghanistan has always been relative; ideal peace would still remain elusive. Future of Afghanistan would largely be driven by fulfilment of international financial commitments for socio-economic development and regional economic connectivity, eventually leading to its economic integration with the regional countries.

Pakistan has hosted largest ever population of refugees from Afghanistan (2.6 M) for almost 4th decade; nearly three afghan generations have born and grown on Pakistan soil. All daily commodities including essential food items flow from Pakistan through both legal and illegal trade routes. 85 % of Afghan exports are through Pakistan while Pakistan’s exports to Afghanistan are merely 15 %[17]. Bulk of the trade is however, informal. International security forces / NATO operating in Afghanistan during last decade or so were mostly supported through Pakistan using its roads /communication infrastructure and seaports.

Afghanistan has a new government in place; albeit shared. After withdrawal of international security forces leaving behind residual footprint, Afghanistan may witness some surge in militancy. Biggest challenge for Mr Ashraf Ghani is to set into motion the reconstruction / rehabilitation phase for which Pakistan’s assistance would be inevitable.

Northern regions of Afghanistan are repository of natural gas reserves of around 5 TCF[18] in addition to expansive minerals, which offer lucrative trade options to regional countries.

Even for India, transit trade through Pakistan has been the most convenient arrangement with Afghanistan. Return of normalcy to Afghanistan and beginning of reconstruction /rehabilitation phase would put added demand on Indian goods necessitating enhancement of the existing arrangement. Notwithstanding, Indian investment or desire for alternatives like Chahbahar Port of Iran, Pakistan virtually remains the most viable option for regional connectivity with Afghanistan.

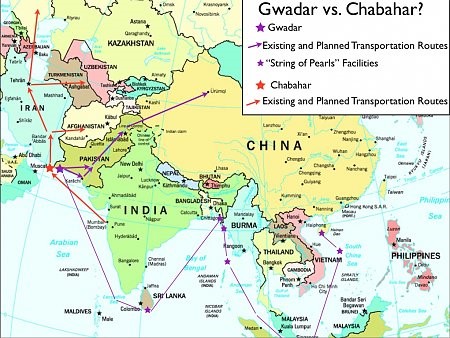

Gwadar vs Chahbahar

Comparing the two (Figure 5[19]), one finds Chahbahar port at a relatively disadvantageous position on two accounts; firstly, its close proximity to the choke point of Strait of Hormuz and shallow waters, and secondly, Pakistan and China share common border and are directly connected through land routes, contrary to India and Iran. Notwithstanding political mileage India enjoys with Iran and Afghanistan, Gwadar offers shortest access to the sea to four CARs (except Turkmenistan) both via Afghanistan and via CPEC (bypassing Afghanistan).

Gwadar is a relatively superior alternative to Dubai, out of choke point of Strait of Hormuz, capable of handling larger cargo ‘S’ class ships /oil tankers. The port will facilitate trade among more than two dozen countries of Persian Gulf, CARs, Iran, Afghanistan, East Africa, Pakistan and China; in addition to European nations. In the strategic domain, the port is likely to serve China more than Pakistan, as it provides a land based oil supply port under a trusted ally.

From Pakistan’s perspective, Gwadar Seaport offers following dividends:-

- Foreign Direct Investment from China would generate economic activity.

- Development of port city and allied infrastructure. Karachi Port and Port Qasim are already working on full capacity; Gwadar would provide the urgently needed alternative.

- Regional connectivity and economic integration; Pakistan’s potential as a transit trade hub /energy corridor would get a substantial boost. Gwadar is expected to capture up to 25 % of national imports / exports by 2020, 15 % of transit trade with CARs, 40 % of transit trade with Afghanistan and 12 % with Xinjiang[20].

- Substantial revenues from transit trade /cargo handling.

- Development of relatively backward and restive province of Balochistan, bringing stability and prosperity. As a domino effect, exploration of vast mineral /energy resources of Balochistan (estimated around 29 TCF of natural gas and 6 Bn Barrels of oil[21] in addition to other costly minerals) are also likely to gain momentum.

- Great boast to Pakistan’s maritime sector; tremendous potential for growth.

- Indirectly, it will be boast other sectors /development activities like services sector, local industries /businesses, housing /communication infrastructure etc.

- Jobs creation /employment opportunities estimated at around two million[22].

- Overall additional revenues estimated around USD 40 – 42 Bn added to national economy[23].

Albeit Gwadar is likely to witness tough competition from other ports like Dubai and Chahbahar. However, projected growth in regional commerce / trade may soon outgrow the combined capacity of all these ports – thus making it a win-win situation for all.

Recommendations

- Maintain strategic balance in relations with US and China.

- Capitalize on rapprochement with Russia and offer trade via CPEC through a trilateral agreement between China – Russia – Pakistan. Capacity building of Pak Railway, acquisition of heavy machinery, revival of steel mill /industry is suggested areas of mutual cooperation.

- Build upon Quadrilateral Trade Agreement between China, Kyrgyzstan, Tajikistan and Kazakhstan (operational since 2004) and expand mutual trade relations through exchanges between business communities of respective countries. Offer for transit trade and access to Arabian sea as well as India through Pakistan be extended to these countries.

- Efforts be made to formalize trade with Afghanistan; trade facilitation /customs offices be established on all formal crossings and trade through these points should be incentivized – subsidize the customs duty /other taxes.

- Manage pending disputes with India till their resolution to create environment for mutual trade for the benefit of people on both sides. India should be encouraged to trade with CARs /Afghanistan through Pakistan and import energy from CARs /Middle East through Pakistan; this will create her stakes in stability of Pakistan.

- Explore avenues with Iran – seek points of convergences.

- It should be promoted via media and other diplomatic channels that Gwadar is a win-win scenario for the region as a whole, as the volume of potential transit trade is expected to be much larger than the combined capacity of Gwadar and Chahbahar seaports.

- Gwadar is not a military outpost of China; misperceptions be cleared loudly and squarely. It is a mutual economic cooperation venture; FDI from other countries like Oman, UAE, Turkey, etc., be encouraged as it would help in clearing misperceptions as well as creating healthy competitive environment.

Regional Connectivity and Trade Facilitation

- Reach out to Neighbouring Countries through:

- Government to government engagements.

- Enter into regional /bilateral transit trade /transportation agreements.

- Mutual interaction within business communities.

- Participate in bilateral /multilateral /regional forums /seminars /expeditions.

- Exchange of visits – government functionaries, business community, intelligentsia.

- Transit trade between Pakistan and its neighbours would require congenial business environment. Introduce conducive trade policies; harmonize trade /simplify customs procedures and institutionalize a business friendly regulatory framework with requisite supportive mechanism to encourage the business community from respective countries.

- Establish one logistic ministry to facilitate trade along transit corridor and resolve issues likely to be confronted by international business community /customers. Transit trade directorate established in FBR may be insignificant in face of anticipated volume of transit trade. Institute a one window mechanism. Model of some developed country (modified to suit own environment) may be replicated.

- Encourage transport companies to explore more avenues of doing businesses and seek opportunities in the new markets through joint ventures /investments in transportation sector.

- Huge volume of cargo is expected to move along transit corridor; Pakistan must therefore plan specialized rail-road services and allied infrastructure to meet the challenge.

- Transportation projects must be analysed critically and prioritized from the perspective of their urgency vis-à-vis affordability /fiscal space; these are often vulnerable to miscalculations and mal-investment. Dead investments driven by purely political considerations (bumper sticker projects) often turn out to be counterproductive – bridges to nowhere; hence must be discouraged ruthlessly.

(End)END NOTES

[1]Stephen P Cohen, quoted in “Pakistan: A Geographical Battlefield” by Mr Ahmed Shaheen, Pak Tribune. Accessed October 5, 2014. http://paktribune.com/articles/Pakistan-A-Geographical-Battlefield-242831.html

[2] Riaz Haq, “Pak-China Industrial Corridor to Boost Pakistan’s FDI, Manufacturing and Exports”, Haq’s Musings (blog), December 10, 2014. Accessed December 26, 2014. http://www.riazhaq.com/2014/12/pak-china-industrial-corridor-to-boost.html

[3] Asim Siddiqui, “Developing the Pak – China Economic Corridor to facilitate Sino – Europe Trade” presented at Intermodal Europe 2014 held at Rotterdam (11-13 November 2014). Accessed December 26, 2014.

http://www.intermodal-events.com/files/aasim_siddiqui.pdf

[4] Munawar Hassan, “Proposed Kashgar – Gwadar Trade Corridor”, The News, September 20, 2013. Accessed December 10, 2014. http://www.thenews.com.pk/Todays-News-3-203063-Proposed-Kashgar-Gwadar-trade-corridor

[5] “China’s share of global gross domestic product (GDP) adjusted for purchasing-power-parity (PPP) from 2010 to 2020 with forecasts until 2026”, Statista, Accessed April 28, 2021.

https://www.statista.com/statistics/270439/chinas-share-of-global-gross-domestic-product-gdp/#:~:text=In%202020%2C%20China%27s%20share%20was%20about%2018.34%20percent.

[6] Asim Siddiqui, “Understanding Economic benefits of Trade corridor between Gwadar – Kashgar Intermodal Network”. Accessed November 30, 2014. http://www.intermodal-asia.com/files/aasim_siddiqui__apsa.pdf

[7] Ibid.

[8] Ibid.

[9] “Pak – China Economic Corridor to help setup new dry ports in country”, Business Recorder, November 25, 2014. Accessed December 10, 2014. http://www.brecorder.com/business-and-economy/189:pakistan/1245377:pak-china-economic-corridor-to-help-set-up-new-dry-ports-in-country/

[10] K M Seethi, “India’s ‘Connect Central Asia’ Policy”, Diplomat, December 13, 2013. Accessed December 7, 2014. http://thediplomat.com/2013/12/indias-connect-central-asia-policy/

[11] Rohit Kumar, “India Pakistan Trade Relations: Current and Potential”, Jinnah Institute, Accessed December 7, 2014. http://jinnah-institute.org/india-pakistan-trade-relations-current-and-potential/

[12] “Geo-Strategic Significance of Pakistan”, CSS Forum, Civil Services of Pakistan. Accessed July 24, 2013. http://www.cssforum.com.pk/css-compulsory-subjects/current-affairs/44753-kips-geo-strategic-importance-pakistan-ms-word-format.html

[13] Dr Shabir Ahmed Khan, “Geo Economic Imperatives of Gwadar Seaport and Kashgar Economic Zone for Pakistan and China”, IPRI Journal XIII, Summer 2013, Accessed December 8, 2014. http://greatgwadar.com/vzpanel/docs/Gwadar%20Sea%20Port%20&%20Kashgar%20Economic%20Zone%20-%20Pakistan%20&%20China.pdf

[14] Termez is the south most city of Uzbekistan.

[15] Dr Zafar Anwar, “Development of Infrastructural linkages between Pakistan and Central Asia”, South Asian Studies, Jan-Jun 2011, Accessed December 7, 2014. http://pu.edu.pk/images/journal/csas/PDF/7-Dr.%20Zahid%20Anwar.pdf

[16] Ibid.

[17] Ibid.

[18] Ibid.

[19] “Chabahar port vs Gwadar port”, Indian Defence Forum. Accessed December 26, 2014. http://defenceforumindia.com/forum/subcontinent-central-asia/5536-chabahar-port-vs-gwadar-port.html

[20] Khan, “Geo Economic Imperatives of Gwadar Seaport and Kashgar Economic Zone for Pakistan and China”.

[21] Anwar, “Development of Infrastructural linkages between Pakistan and Central Asia”.

[22] Mehmood ul Hassan, “Pak-China Friendship: New Dimensions and New Opportunities”, Overseas Pakistani Friends, March 25, 2013.Accessed December 11, 2014. http://www.opfblog.com/13906/pak-china-friendship-new-dimensions-and-new-opportunities/

[23] Ibid.

Farzana Shah is editor @ Global Conflict Watch. She is a Journalist/DEFENSE & Cortex analyst, Geo Strategic & Geopolitical Affairs commentator with special focus on militancy along Pak-Afghan border region, terrorism and Indo-Pak relations. She is based in Peshawar and is recipient of International Award in Journalism. Furthermore, she has contributed to significant national/ international newswires on regional / domestic geopolitics, security and threats. She tweets @Jana_Shah.

Comments